Exit Strategies in Private Equity: Maximizing Returns

Learn private equity strategies for exits through IPOs, strategic sales, mergers, or secondary sales, using Haptiq’s Olympus to time markets and maximize portfolio value.

Private equity (PE) exits are the pivotal moments where investment strategies culminate in financial returns. Because PE stakes are inherently illiquid, a clear exit plan isn't optional—it is the only way investors turn paper value into cash. Whether through IPOs, strategic sales, mergers, or secondary deals, exits are the culmination of meticulous work designed to maximize portfolio value. Success hinges on timing markets, preparing companies operationally, and choosing the right path to unlock a portfolio's full potential.

From sector booms to buyer appetite, firms that master private equity exit strategies turn portfolios into windfalls. This article explores the art and science of PE exits—covering every major exit route, the decision framework behind choosing one, and how tools like Haptiq's Olympus help firms execute with precision.

Consider the story of ServiceMax, sold by Silver Lake to PTC for ~$1.46 billion in 2022 after years of cloud platform investment and margin improvement. That outcome didn't happen by accident—it was the product of deliberate operational preparation, market timing, and a compelling buyer narrative. That's the playbook this article unpacks.

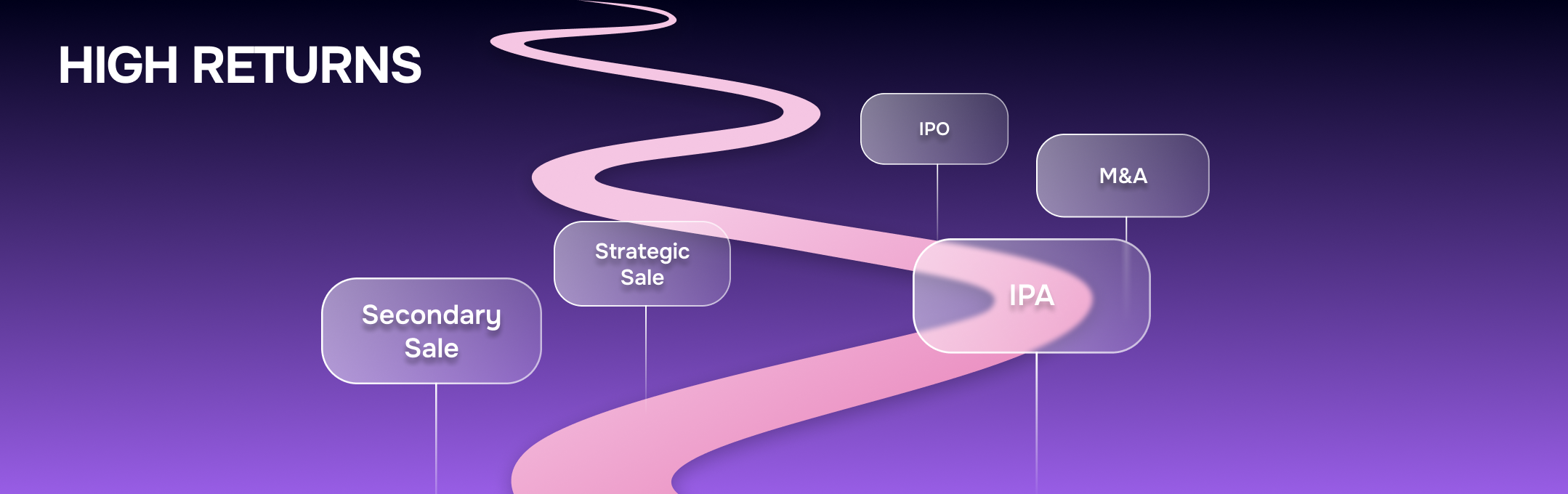

Exit Strategies in Private Equity

Exit strategies are where long-term value creation efforts translate into tangible returns for LPs and GPs alike. Whether through IPOs, strategic sales, mergers, secondary deals, management buyouts, or recapitalizations, exits require meticulous timing, preparation, and execution to achieve optimal outcomes.

The right exit path depends on a company's maturity, market position, buyer appetite, and the fund's timeline. Each route carries its own complexity, speed, and valuation dynamics—and the best firms think about exit optionality from day one of ownership.

Common exit strategies

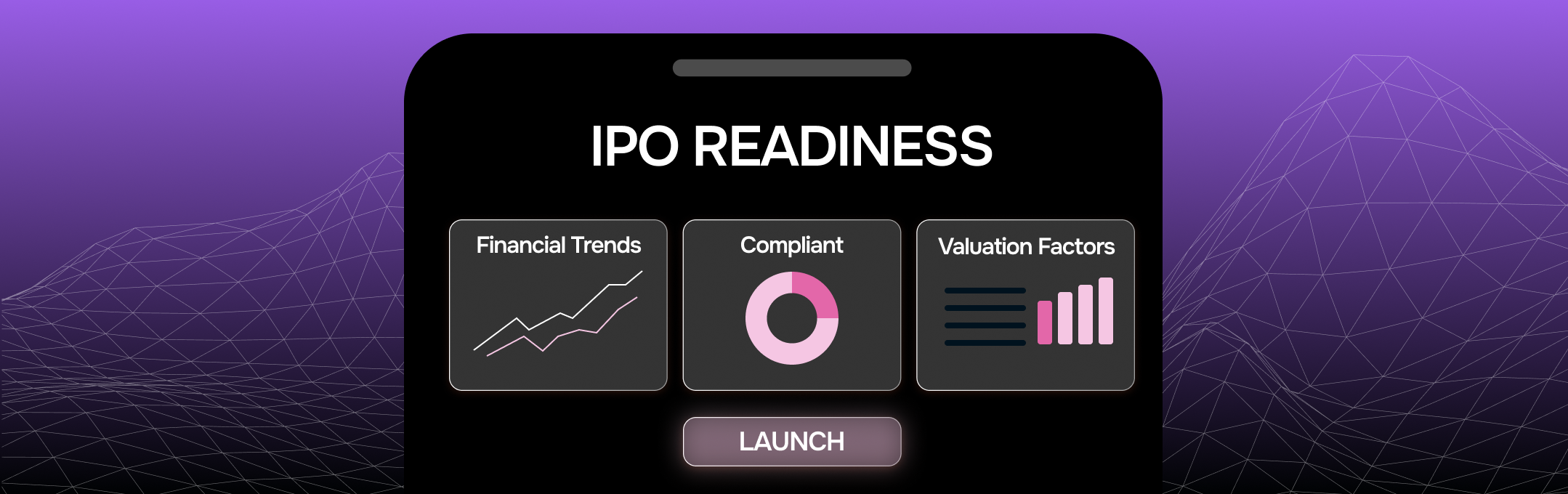

1. Initial public offering (IPO)

An IPO gives a PE-backed company access to public market capital and broad investor visibility. It's often the highest-profile exit route, but also the most demanding to execute.

- Market readiness: Firms build robust financials and compelling growth stories to attract institutional investors. A strong management team, clear competitive differentiation, and sustainable revenue models are non-negotiable. Sectors like technology and healthcare tend to command premium multiples when market sentiment is favorable.

- Compliance burden: Public markets require transparent governance, audited financials, and detailed disclosures. Meeting these standards demands significant legal, advisory, and reporting discipline—any lapse risks delays that can erode investor confidence.

- Valuation upside: In thriving markets, IPOs can unlock substantial value—particularly for companies in high-growth industries. Timing the launch to align with market enthusiasm is critical to securing strong demand and favorable pricing.

IPOs suit fast-growing firms with scalable models, like software or biotech companies. They require precise coordination across pricing, investor roadshows, and underwriter selection. Firms that invest early in governance and financial infrastructure tend to execute smoother transitions to public ownership.

2. Strategic sale

Selling to a larger corporation is often the most efficient private equity exit strategy, particularly when the buyer has a clear strategic rationale for the acquisition.

- Speed: Strategic sales close faster than IPOs, allowing firms to seize favorable market windows. Targeting buyers with strong strategic alignment ensures efficient negotiations and preserves value before conditions shift.

- Synergies: Buyers pay premiums for companies that enhance their operations—whether through complementary technology, customer networks, or geographic reach. Firms that can quantify synergy value in the buyer's language tend to attract more competitive bids.

- Negotiation leverage: Running a structured process with multiple potential buyers creates competitive tension. Advisors who can articulate a company's unique strengths—proprietary products, high retention, defensible market position—drive offers that reflect full potential.

Strategic sales fit companies with clear corporate appeal: niche technology providers, specialized manufacturers, or consumer brands with loyal customer bases. They excel when buyer synergies outweigh the complexity and cost of a public offering.

3. Merger or Acquisition (M&A)

Merging with or acquiring another business creates value through combined scale and operational synergies, often positioning the combined entity for a larger exit down the road.

- Operational fit: The strongest M&A outcomes come from partners with complementary capabilities—aligned supply chains, shared technology infrastructure, or overlapping customer segments. Thorough diligence on cultural and operational compatibility minimizes integration risk.

- Scale advantage: Larger, more diversified businesses attract broader buyer interest and command stronger multiples from both strategic acquirers and public markets. Scale also strengthens negotiating power in future exit processes.

- Complex integration: Unifying operations, systems, and cultures requires detailed planning and disciplined execution. Firms that invest in integration management—prioritizing talent retention, technology alignment, and KPI standardization—are far more likely to realize the promised synergies.

M&A exits suit companies in fragmented industries like logistics, healthcare services, or business services, where consolidation creates meaningful competitive advantages. Haptiq's AI platforms for post-merger integration help PE-backed companies accelerate integration timelines and protect value during the critical post-close period.

4. Secondary sale

Selling to another PE firm or financial sponsor is a flexible exit strategy that provides liquidity while preserving upside for a company that isn't yet ready for a strategic or public exit.

- Flexibility: Secondary sales suit companies that need more time to scale, avoiding premature exits at lower valuations. Targeting buyers with sector expertise ensures strategic continuity and supports long-term growth plans.

- Fresh capital: New owners bring additional capital for expansion—new markets, product development, or debt reduction—that sets the stage for a larger exit in the next cycle.

- Valuation gains: Improved operational performance, stronger market positioning, and demonstrated growth metrics attract higher offers. Secondary sales effectively bridge value creation across investment cycles.

Secondary sales are common for mid-cycle companies in technology, healthcare, or consumer sectors where the growth story is compelling but the business isn't yet ready for a strategic buyer or public markets.

5. Management buyout (MBO)

A management buyout involves selling all or a significant portion of the company back to its existing leadership team, often with financial sponsor backing. MBOs are a compelling exit option when management has deep operational knowledge and a strong conviction in the business's future.

- Alignment: Management teams with skin in the game are highly motivated to drive performance post-transaction, which can accelerate value creation.

- Continuity: MBOs minimize disruption to operations, culture, and customer relationships—a meaningful advantage for businesses where relationships and institutional knowledge are core assets.

- Financing complexity: MBOs typically require a combination of management equity, PE co-investment, and debt financing. Structuring the deal to align incentives while managing leverage is critical to a successful outcome.

MBOs work best in stable, cash-generative businesses where management has a clear operational vision and the market doesn't yet support a premium strategic or public exit.

6. Recapitalization (dividend recap)

A recapitalization doesn't transfer ownership but allows the fund to realize cash today by having the portfolio company take on additional debt and distribute the proceeds as a dividend. It's a way to return capital to LPs while retaining ownership and future upside.

- Partial liquidity: Recaps let firms lock in some returns without fully exiting, preserving the option to pursue a larger exit when conditions improve.

- Leverage risk: Adding debt to a portfolio company increases financial risk. Recaps work best for businesses with strong, predictable cash flows that can comfortably service the additional debt load.

- LP relations: Returning capital mid-hold demonstrates active portfolio management and can strengthen LP relationships ahead of future fundraising.

Recaps are most appropriate for mature, cash-generative businesses where the PE firm has high conviction in continued performance but wants to reduce unrealized exposure.

How PE firms decide which exit path to use

Choosing the right exit strategy isn't formulaic—it requires synthesizing multiple factors simultaneously:

The best PE firms don't wait until year four or five to think about exit optionality. They build exit-readiness into the value creation plan from day one—ensuring the company's financial profile, operational infrastructure, and growth narrative are compelling across multiple exit scenarios simultaneously.

Timing and execution

Successful private equity exit strategies depend as much on when you exit as how you exit. Firms that get the timing right consistently outperform those that don't.

- Market timing: Exiting during industry upswings—technology booms, healthcare consolidation waves, or favorable credit markets—maximizes buyer interest and valuation multiples. Firms that monitor economic cycles and sector-specific signals can identify optimal windows before they close.

- Financial strengthening: Enhancing EBITDA margins, revenue quality, and working capital efficiency in the 12–24 months before exit makes companies significantly more attractive to buyers and public market investors. Operational improvements like AI-driven automation, customer retention programs, and supply chain optimization directly translate into higher exit multiples.

- Narrative building: Buyers and investors don't just buy financials—they buy stories. Compelling narratives around market leadership, innovation, and defensible competitive position captivate buyers and public markets alike. Firms that back their narratives with robust data—customer retention rates, NPS scores, product roadmaps—command premium valuations.

Thorough preparation prevents undervalued exits. Haptiq's Olympus provides real-time operational insights and portfolio analytics that help PE firms identify value creation levers, monitor exit readiness, and execute with precision.

Illustrative Exit Examples

The following scenarios illustrate how private equity exit strategies play out in practice, using representative figures to clarify key concepts.

IPO playbook (tech portco)

- Multi-year investment in financial controls, governance infrastructure, and management team depth

- New product launches drive steady revenue acceleration, expanding the addressable market

- Market-peak timing captures a 25× earnings multiple at pricing

- Outcome: Outsized valuation, liquid shares for the fund, and a management team positioned for continued public market success

Strategic sale (specialty manufacturer)

- Buyer seeks supply-chain synergies and customer overlap with existing portfolio

- Deal thesis anchored on multimillion-dollar annual cost savings and high customer retention

- Competitive process with multiple strategic bidders drives a premium offer

- Outcome: Fast close during an industry upswing, maximizing proceeds through strategic alignment

Secondary sale (SaaS platform)

- Company has strong product-market fit but needs additional capital and operational expertise to scale internationally

- New PE sponsor brings sector-specific experience and a global network

- Fresh capital funds for international expansion and product development

- Outcome: Valuation step-up at secondary close, with a clear path to a strategic exit in the next cycle

Conclusion

Private equity exit strategies—IPOs, strategic sales, M&A, secondary sales, MBOs, and recapitalizations—convert years of operational work into meaningful returns for investors. The difference between a good exit and a great one comes down to preparation, timing, and the quality of the story you can tell.

Firms that build exit-readiness into their value creation plans from day one, invest in operational infrastructure that drives measurable EBITDA improvement, and monitor market conditions with real-time data consistently outperform those that treat exits as an afterthought.

Haptiq's Olympus platform is purpose-built to support PE firms and their portfolio companies through every stage of the investment lifecycle—from post-acquisition integration to exit preparation. If you're thinking about how to maximize value at exit, let's talk.

FAQs

1) What are the main exit strategies in private equity?

The primary private equity exit strategies are: initial public offerings (IPOs), strategic sales to corporate acquirers, mergers and acquisitions (M&A), secondary sales to other financial sponsors, management buyouts (MBOs), and recapitalizations. Each route offers a different balance of speed, valuation potential, and complexity. The right choice depends on the company's maturity, market conditions, and the fund's timeline and return objectives.

2) How do private equity firms decide which exit path to use?

PE firms evaluate several factors simultaneously: current market conditions and sector multiples, the company's financial and operational readiness, the available buyer universe, valuation expectations relative to comparable transactions, process complexity and cost, and the fund's remaining life. The best firms build exit optionality into their value creation plans from day one, ensuring the company is compelling across multiple exit scenarios. Tools like Haptiq's Olympus Portfolio Management help firms monitor portfolio readiness and identify optimal exit windows in real time.

3) What is a secondary sale, and when is it used?

A secondary sale occurs when a PE firm sells its stake in a portfolio company to another financial sponsor rather than to a strategic acquirer or the public market. It's typically used when: the company needs more time to scale before a strategic or public exit, the fund is approaching the end of its life and needs to return capital to LPs, or a new sponsor with different expertise can unlock additional value. Secondary sales provide liquidity while preserving upside, and often serve as a bridge to a larger exit in the next investment cycle.

4) How do IPOs fit into private equity exit strategies?

IPOs are a high-profile exit route that gives PE-backed companies access to public market capital and broad investor visibility. They tend to deliver the highest valuations in favorable market conditions, particularly for fast-growing companies in technology or healthcare. However, they require years of preparation—building governance infrastructure, audited financials, and a compelling investor narrative—and are highly sensitive to market timing. IPOs work best for companies with scalable business models, strong management teams, and a clear growth story that resonates with institutional investors.

5) Why are strategic sales effective private equity exit strategies?

Strategic sales connect PE-backed companies with corporate buyers who have a clear rationale for the acquisition—whether that's technology capabilities, customer access, geographic expansion, or operational synergies. Because buyers can quantify the value of those synergies, they're often willing to pay premium prices. Strategic sales also close faster than IPOs and bypass the regulatory complexity of public markets, making them a reliable and efficient exit route for companies with clear corporate appeal.

6) What makes timing critical in private equity exit strategies?

Timing is one of the most significant drivers of exit value. Exiting during industry upswings—when sector multiples are elevated, buyer appetite is strong, and credit markets are favorable—can add meaningful percentage points to exit multiples. Conversely, exiting into a downturn or a period of market uncertainty can significantly compress valuations. Firms that monitor economic cycles, sector-specific signals, and buyer activity in real time are best positioned to identify and act on optimal exit windows before they close.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.svg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)